When pulling down a new job offer or looking to transition your career, one of the most critical decisions you will face isn’t just about the base pay rate—it’s about how that income is classified. Choosing between a traditional W2 employee role and a 1099 independent contractor agreement fundamentally changes your tax landscape, take-home pay, and compliance requirements.

At Savvy Tax Group, we frequently speak with professionals who are shocked when their first tax bill arrives because they didn’t fully grasp the underlying W2 vs 1099 tax differences. Let’s break down the rules, look at the pros and cons of each side, and reveal how to avoid the hidden tax traps that catch millions of workers off guard.

The Core Difference: How Uncle Sam Views Your Income

The IRS looks at W2 employees and 1099 independent contractors through entirely different lenses. It all boils down to behavioral control, financial control, and the nature of the relationship:

- W2 Employee: You work for an employer who dictates when, where, and how you work. In return, your employer handles tax withholding directly from your paycheck.

- 1099 Contractor: You are self-employed. You run your own business, set your own hours, and provide services to clients. Crucially, no taxes are withheld from your checks; you are paid the gross amount.

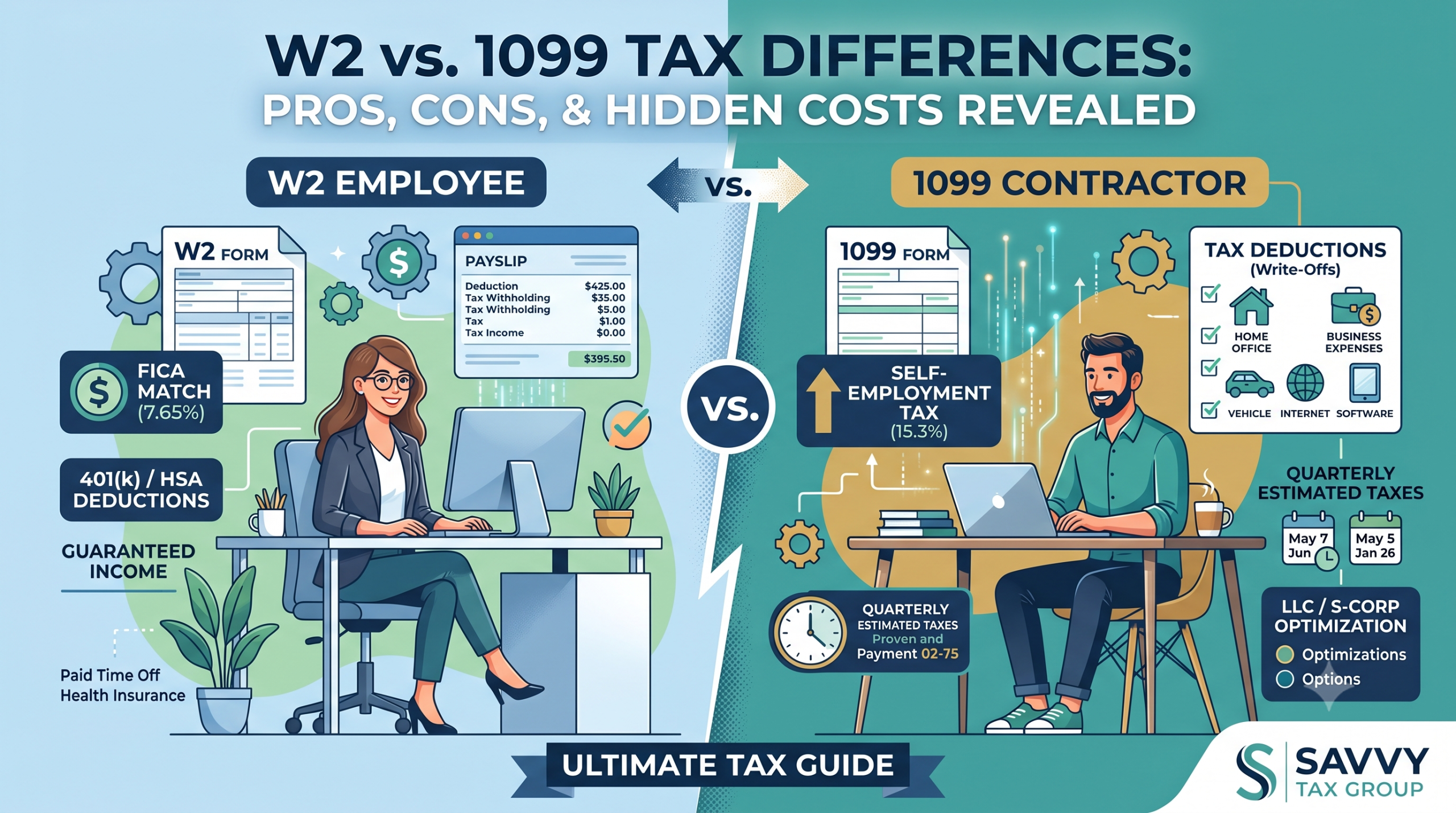

The W2 Employee Tax Landscape: Stability and Shared Costs

Being a W2 employee is the standard path for a reason: the tax compliance is automated, and your employer acts as a financial cushion for payroll taxes.

The Pros of W2 Taxes

- The Employer FICA Match: This is the single biggest tax benefit of a W2 role. Total FICA taxes (Social Security and Medicare) amount to 15.3%. As a W2 worker, you only pay half (7.65%), while your employer legally matches and pays the other 7.65%.

- Automated Withholding: Your tax obligations are sliced out of every paycheck via your W-4 form. You don’t have to worry about writing a massive check to the IRS at the end of the quarter.

- Pre-Tax Benefits: You can often slash your taxable income by contributing to employer-sponsored 401(k) plans, Health Savings Accounts (HSAs), and pre-tax health insurance premiums.

The Cons of W2 Taxes

- Zero Write-Off Flexibility: Ever since the Tax Cuts and Jobs Act (TCJA), W2 employees can no longer deduct unreimbursed employee expenses. If you buy your own laptop for work, pay for your own continuing education, or drive for company business without reimbursement, you cannot write those expenses off on your tax return.

The 1099 Contractor Tax Landscape: Total Control and Write-Off Wealth

As a 1099 independent contractor, you aren’t just an individual worker anymore—you are a business entity in the eyes of the IRS, even if you operate as a sole proprietor.

The Pros of 1099 Taxes

- Unlocking Powerful Tax Deductions: This is where 1099 workers win big. You can write off ordinary and necessary business expenses to drastically reduce your adjusted gross income (AGI). High-value independent contractor tax deductions include home office expenses, internet and phone bills, software, advertising, business travel, and vehicle costs.

- The QBI Deduction (Qualified Business Income): Under current tax laws, eligible 1099 contractors can deduct up to 20% of their business net income right off the top before standard tax rates are applied.

- Advanced Retirement Accounts: You can open a SEP IRA or a Solo 401(k), allowing you to tuck away significantly more pre-tax income than a typical W2 employee.

The Cons of 1099 Taxes

- The Self-Employment Tax Trap: Remember the 15.3% FICA tax mentioned earlier? As a 1099 contractor, you are both the employer and the employee. You have to pay the full 15.3% self-employment tax on your net earnings. While you do get an above-the-line deduction for the employer portion, it remains a steep financial hurdle.

- Estimated Quarterly Taxes: Because no one is withholding taxes for you, the IRS requires you to calculate and submit payments four times a year (April, June, September, and January). Fail to do this, and you’ll face underpayment penalties.

- Administrative and Compliance Costs: You are responsible for keeping spotless financial records, tracking receipts, and filing complex schedules (like Schedule C) with your annual return.

W2 vs 1099 Tax Quick Comparison

| Tax Feature | W2 Employee | 1099 Independent Contractor |

| Tax Withholding | Automatic; pulled from every paycheck based on Form W-4. | None; you receive 100% of gross revenue and must pay manually. |

| FICA / Payroll Tax | You pay 7.65%; employer pays the other 7.65%. | You pay the full 15.3% Self-Employment Tax. |

| Business Write-offs | Not allowed for job-related expenses. | Fully allowed for all legitimate business operating expenses. |

| Payment Schedule | Annual filing by April 15. | Quarterly Estimated Taxes + Annual Filing. |

The True Math: Why a $50/hr 1099 Rate is NOT the Same as a $50/hr W2 Salary

A common mistake professionals make is accepting a 1099 contract rate that mirrors a traditional W2 salary. To break even on a 1099 contract due to the self-employment tax vs W2 dynamics, lack of paid time off, and corporate benefits, your 1099 hourly rate generally needs to be 25% to 40% higher than a comparable W2 rate.

For example, if you make $50/hour as a W2 employee, your 1099 vs W2 calculator tax math means you need to bill roughly $65 to $70/hour as a 1099 contractor just to break even after factoring in your self-employment taxes, health insurance premiums, and administrative overhead.

Don’t Guess on Your Taxes—Let Savvy Tax Group Do the Math

Whether you’re trying to figure out if a 1099 contract offer makes financial sense, want to set up an LLC or S-Corporation to lower your self-employment taxes, or need a bulletproof strategy for your quarterly estimated payments, we are here to help. At Savvy Tax Group, LLC, we handle the complex math so you can maximize your take-home pay.

Ready to optimize your tax return? Contact us today to schedule a consultation and make sure you keep more of what you earn.