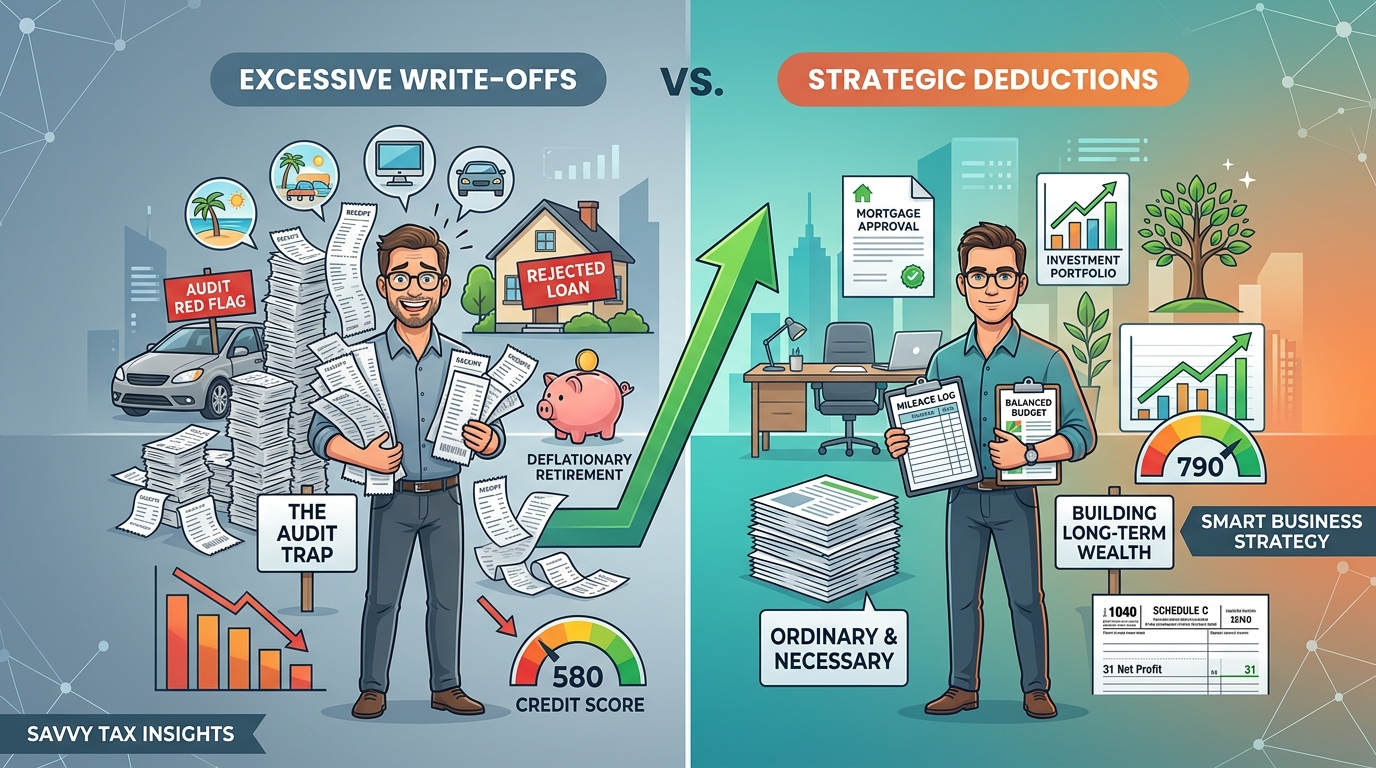

It’s the ultimate water-cooler advice for small business owners, freelancers, and independent contractors: “Just write it off!” From your morning coffee to your latest home tech upgrade, there’s a common belief that running every conceivable expense through your business is the gold standard of financial savvy. After all, lower net income equals fewer tax dollars paid to Uncle Sam on your Schedule C (Form 1040). Right?

While maximizing legitimate business deductions is vital, chasing a “zeroed-out” bottom line can backfire dramatically. For sole proprietors and single-member LLCs, the net profit reported on your tax return isn’t just a number the IRS looks at—it is the official financial report card of your livelihood. Aggressively writing off personal or borderline expenses can jeopardize your financial future in ways you might not expect.

1. The Lending Trap: Why Your Bank Says “No”

When you file a Schedule C, your net profit (Line 31) flows directly onto your personal Form 1040 as your taxable earned income. If you write off every meal, mileage point, and personal gadget to minimize that number, you look fabulously lean to the IRS. However, you look completely broke to a mortgage officer or business lender.

When applying for a home loan, an auto lease, or a business line of credit, underwriters calculate your Debt-to-Income (DTI) ratio based on that exact net profit line—not your gross revenue. If your business brought in $120,000 but you aggressively claimed $100,000 in “write-offs,” a bank views your annual income as $20,000. That dream of purchasing a home or upgrading your commercial space could instantly vanish because, on paper, you don’t earn enough to cover the payments.

💡 Savvy Strategy: If you plan to buy a home or secure a commercial loan within the next 24 months, it is often wise to work with a CPA to consciously balance your deductions. Sometimes, paying a bit more in self-employment tax today is the key to unlocking major financing tomorrow.

2. Underfunding Your Future: The Social Security Squeeze

As a self-employed individual, you pay a 15.3% Self-Employment (SE) tax on your net earnings. This tax directly funds your future Social Security and Medicare benefits. While eliminating this tax liability feels like an immediate win, you are effectively reducing your future safety net.

The Social Security Administration calculates your retirement benefit based on your top 35 years of earned income. Consecutive years of reporting near-zero net profits on your Schedule C mean you are contributing nothing to the system—which guarantees a minimal payout when it’s time to retire. Defunding your own future to save a few tax dollars today is an expensive trade-off.

3. The IRS Audit Radar: Green Flags vs. Red Flags

The IRS uses sophisticated automated algorithms—specifically the Discriminant Inventory Function (DIF) score—to compare your Schedule C line items against industry averages. If your deductions are completely out of proportion with your revenue or peers, your return gets flagged for human review.

| High-Risk Deduction (The “Write-Off” Red Flags) | The Strategic Reality |

| 100% Business Use of Personal Vehicle | Claiming your sole personal car never travels for groceries or family trips is an instant flag. It must be backed by an impeccable, contemporaneous mileage log tracking dates, destinations, and business purposes. |

| Excessive Travel & Meals | Claiming every single weekend dinner or casual outing as a client consultation. The IRS requires expenses to be ordinary, necessary, and documented with names and specific business agendas. |

| Perpetual Net Losses | Reporting a net loss on Schedule C year after year. If you don’t show a profit in 3 out of 5 consecutive years, the IRS can reclassify your business as a Hobby. |

4. The Hobby Loss Rule: Guard Your Business Status

Under Internal Revenue Code Section 183, a legitimate business must demonstrate a clear intent to make a profit. If you consistently use excessive write-offs to generate a tax loss, the IRS may declare your venture a hobby. If your business is reclassified as a hobby:

- You must still report and pay tax on 100% of your gross revenue.

- You lose the ability to deduct any business expenses against that revenue under current tax law.

- You open previous tax years up to audits, back taxes, and heavy interest penalties.

Finding the Sweet Spot: Strategic Deduction

The goal of professional tax planning isn’t simply to minimize taxes at all costs—it is to maximize your wealth accumulation and business value. To achieve this balance, shift your mindset from “writing everything off” to “strategic record-keeping”:

- Separate Personal and Professional: Maintain completely distinct bank accounts and credit cards. Never blend personal expenses with business tracking.

- Understand “Ordinary and Necessary”: To be deductible, an expense must be standard in your industry and helpful to running your business. If it doesn’t directly contribute to generating revenue, leave it out.

- Align with Your 3-Year Goals: If you need credit or a mortgage soon, plan for profitability. If you are established and fully liquid, look to legally defer income or leverage tax-advantaged retirement accounts (like a SEP IRA or Solo 401k) rather than inflating everyday write-offs.

Building a Savvy Foundation

A zero-dollar tax bill might feel victorious in April, but it shouldn’t come at the cost of your creditworthiness, your retirement security, or your peace of mind during an audit. True business growth means generating real, visible, documented profit. When you are ready to stop guessing and start scaling strategically, consulting a certified professional can help ensure your Schedule C reflects a business built to last.