Cryptocurrency has taken the financial world by storm. Whether you are actively trading Bitcoin, exploring Ethereum, or just dipping your toes into the crypto waters, it is an exciting space.

However, there is one crucial partner that follows your digital coins wherever they go: the IRS. Tax rules around digital assets can seem incredibly confusing, but they don’t have to be. Let’s break down the absolute basics of cryptocurrency taxes in plain, simple English—no accounting degree required.

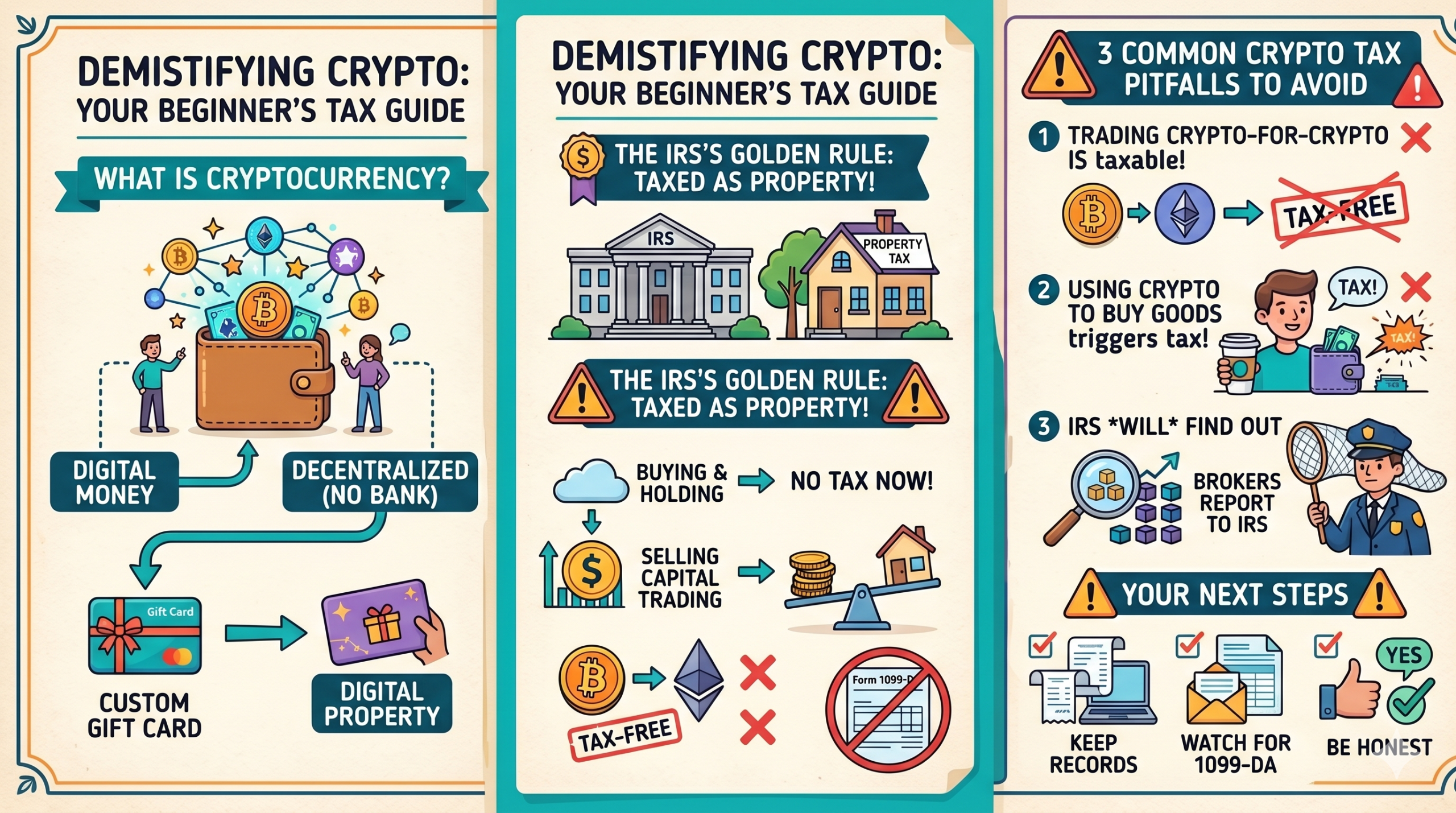

The Golden Rule: Crypto is Property, Not Cash

To understand how cryptocurrency is taxed, you have to understand how the government views it. The IRS does not treat crypto like regular money (such as the U.S. dollar). Instead, they classify cryptocurrency as property.

Non-Taxable Events: When You Don’t Owe Anything

The good news is that simply looking at crypto or moving it around doesn’t automatically mean you owe the government money. You generally do not have to pay taxes when you:

- Buy crypto with cash: Buying Bitcoin or any other coin with U.S. dollars is not a taxable event. You just hold onto it.

- Transfer crypto between your own wallets: Moving your digital assets from an exchange (like Coinbase) to your personal digital wallet doesn’t trigger a tax bill. You are just moving your own property from one pocket to another.

Taxable Events: When the IRS Wants a Cut

Taxes kick in when you “dispose” of your cryptocurrency. This is where capital gains and losses come into play. You are triggering a taxable event if you:

1. Sell Crypto for Cash

If you buy $1,000 worth of crypto and later sell it for $3,000, you have a $2,000 capital gain. You will owe taxes on that $2,000 profit. If you sell it for less than you bought it for, you have a capital loss, which can actually help lower your overall tax bill.

2. Trade One Crypto for Another

This is a trap that catches many beginners. If you swap your Bitcoin directly for Ethereum, the IRS views that as a two-step process: you “sold” your Bitcoin for its cash value, and then used that cash to buy Ethereum. If your Bitcoin gained value since you bought it, you owe taxes on that gain—even though you never withdrew actual cash to your bank account.

3. Spend Crypto to Buy Goods or Services

Using crypto to buy a cup of coffee, a laptop, or a car counts as selling your crypto. If the value of the crypto you spent went up from the time you originally acquired it, that transaction triggers a taxable capital gain.

How Much Will You Be Taxed?

The tax rate you pay depends entirely on how long you held the cryptocurrency before selling or trading it:

- Short-Term Capital Gains (1 Year or Less): If you hold your crypto for a year or less before selling or trading it, your profits are taxed at your regular income tax rate. This rate is usually higher.

- Long-Term Capital Gains (More Than 1 Year): If you hold your crypto for more than a year, you qualify for lower long-term capital gains tax rates. Patience literally pays off here.

Crypto Earned as Ordinary Income

Sometimes, you don’t buy crypto; you earn it. If you receive cryptocurrency from mining, staking rewards, airdrops, or as payment for work, it is taxed immediately as ordinary income.

You must report the fair market value of the coins in U.S. dollars on the exact day you received them. That value becomes your “cost basis” if you decide to sell the coins later down the road.

The Infamous “Crypto Question” on Form 1040

Do not try to hide your crypto activity from the IRS. Every single person filing a standard individual tax return must answer a mandatory, explicit question at the top of Form 1040. You must check “Yes” or “No” honestly.

| Action | How to Answer the IRS Question |

|---|---|

| Only bought crypto with cash | Check “No” (as long as you didn’t sell or trade any) |

| Moved crypto between your own wallets | Check “No” |

| Sold crypto, swapped coins, or earned staking rewards | Check “Yes” |

Tips to Keep Tax Season Stress-Free: Always track your “Cost Basis” (what you paid for it plus fees). Look out for Form 1099-DA from your brokers or exchanges. If you trade frequently, consider using crypto tax software to link your wallets and calculate your gains automatically.

Disclaimer: This post provides a basic overview of digital asset taxation for educational purposes. Because crypto regulations are constantly evolving, it’s always a smart move to chat with a certified tax professional regarding your specific situation.