Thinking about saving for the future can sometimes feel overwhelming, especially when terms like “tax-advantaged accounts” and “contribution limits” get thrown around. But building a comfortable retirement doesn’t require a degree in finance or accounting.

One of the easiest and most effective tools available to everyday savers is the Traditional Individual

Retirement Account (IRA). In this quick guide, we’re breaking down the core benefits of a Traditional IRA

in plain English—explaining exactly how it keeps more money in your pocket today while fueling your dreams

for tomorrow.

What is a Traditional IRA and How Does It Work?

At its heart, a Traditional IRA is simply a specialized personal savings account that gives you distinct tax breaks for setting money aside for retirement. Unlike a workplace 401(k), you open a Traditional IRA yourself through a bank, brokerage, or investment app.

Anyone who has earned income (money from a job or business endeavor) can open and contribute to a Traditional IRA. Think of it as an exclusive piggy bank where the government rewards you for every dollar you drop inside.

Tip for the Reader: If you’re wondering how a traditional IRA works mechanically, think of it as a

financial shield that protects your retirement money from taxes while it grows.

Benefit 1: An Immediate Tax Break (The Traditional IRA Tax Deduction)

The most immediate and celebrated perk of a Traditional IRA is the ability to deduct your contributions from your federal income taxes. This directly reduces your Adjusted Gross Income (AGI) for the year.

Let’s look at a simple example. Suppose your annual earned income is I = $60,000. If you contribute C = $5,000 to your Traditional IRA this year, the IRS will calculate your income tax as if you only made: Taxable Income = I − C = $60,000 − $5,000 = $55,000

Because you are deducting that $5,000 from your taxable pool, you instantly pay less money to Uncle Sam during tax season. You are essentially keeping that tax money for yourself and letting it build your own wealth instead.

A Quick Note on Income Limits

If you or your spouse have a retirement plan at work (like a 401k), the IRS might limit how much of your IRA contribution you can deduct if your income is above certain thresholds. However, if neither of you has a workplace plan, you can take the full deduction no matter how much money you make!

Benefit 2: Tax-Deferred Growth (The Snowball Effect)

When you invest money in a standard, everyday brokerage account, you typically have to pay taxes every single year on any dividends or capital gains your investments earn. This annual tax bill acts like friction, slowing down your wealth creation.

Inside a Traditional IRA, your investments enjoy tax-deferred growth. This means you don’t pay a single penny in taxes on investment growth, interest, or dividends as long as the money remains in the account.

Because no money is being stripped away each year to pay taxes, your interest compounds faster. Your gains generate their own gains, creating a powerful financial snowball effect over decades.

Benefit 3: Lower Tax Brackets in Retirement

Eventually, when you reach retirement age (specifically age 591⁄2 or older), you will start taking money out of your Traditional IRA to fund your lifestyle. These withdrawals are taxed as regular income.

Why is this a major benefit? Most people find themselves in a lower tax bracket during retirement than they were during their peak earning years. By shifting your tax burden from your high-income youth to your lower-

income retirement years, you naturally end up paying a smaller overall percentage of your money to taxes.

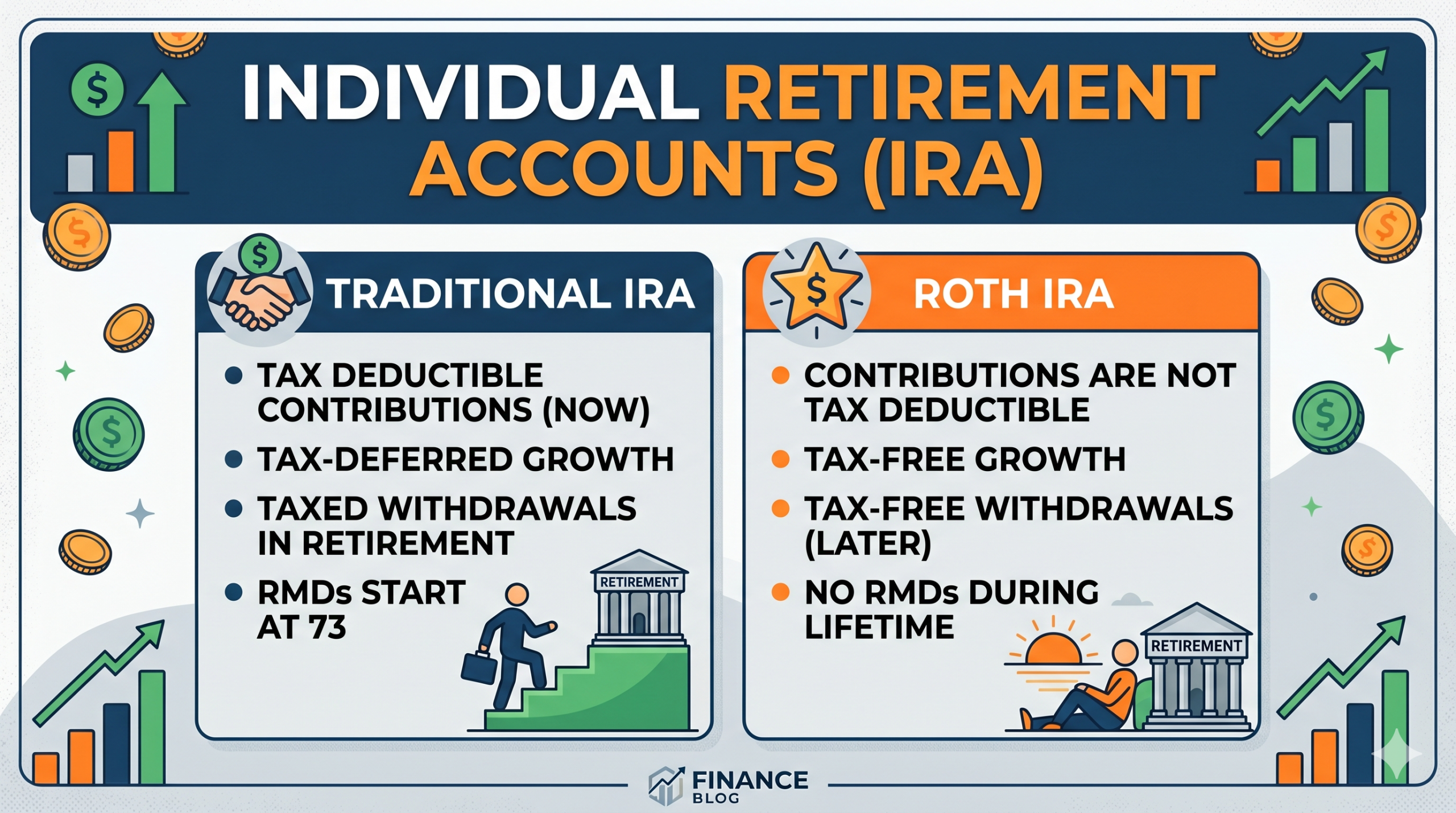

Traditional IRA vs. Roth IRA: What’s the Difference?

You can’t talk about a Traditional IRA without mentioning its famous sibling, the Roth IRA. The choice boils down to a simple question of timing:

- Traditional IRA: You get a tax break now when you contribute, and pay taxes later when you withdraw.

- Roth IRA: You pay taxes now (no deduction), but your withdrawals are 100% tax-free later.

If you think your tax rate is higher today than it will be in the future, the Traditional IRA is generally your best

option.

How to Start Maximizing Your Retirement Savings

Getting started is incredibly simple and takes less than 15 minutes:

- Choose a Provider: Pick an online brokerage, automated investing platform (robo-advisor), or local bank.

- Open the Account: Select “Traditional IRA” as the account type.

- Link Your Bank Account: Set up a one-time transfer or establish automated monthly contributions to

build consistent habits. - Select Your Investments: Remember, opening the account is just step one! You must choose where to

allocate that money (such as target-date funds or low-cost index funds) so it can start growing.

Frequently Asked Questions (FAQ)

Can I contribute to a traditional IRA if I have a 401(k) at work?

Yes! You can absolutely contribute to both. However, depending on your income level, your ability to deduct your Traditional IRA contributions on your tax return might be reduced or phased out.

What is the penalty for withdrawing money early from a Traditional IRA?

Because these accounts are meant for retirement, taking money out before you turn 59 1⁄2 generally triggers a 10% IRS early-withdrawal penalty, plus regular income taxes on the amount withdrawn. There are exceptions for major life events, like buying your first home or paying for higher education.

Is there a deadline for making Traditional IRA contributions?

One of the best benefits of a Traditional IRA is that you have until the official tax filing deadline (usually April 15th of the following year) to make contributions and count them toward your previous year’s tax deduction.

Contact us Today!

If you are interested in what the tax effect of contributing to an IRA would be for you, contact us today and we will be happy to discuss your tax situation and if a Traditional or Roth IRA would be right for you!